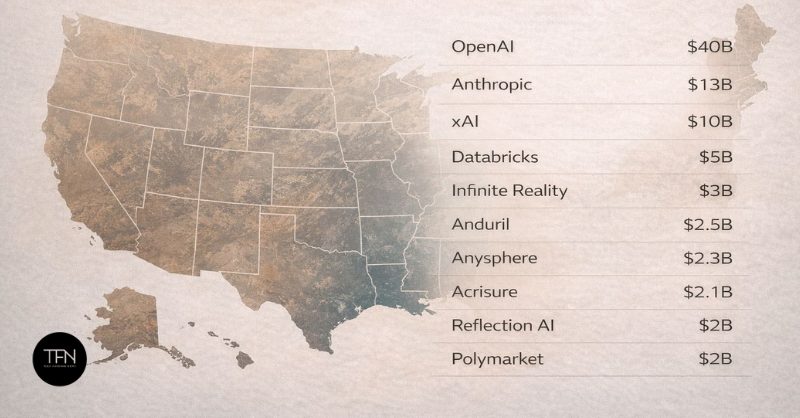

US companies post blockbuster funding rounds in 2025

US startups and high-growth private companies are already logging some of the year’s largest venture and growth-equity financings, underscoring how investor appetite has shifted from broad-based experimentation to fewer, larger bets. The biggest rounds in 2025 are concentrating in capital-intensive categories such as artificial intelligence infrastructure, defense and aerospace, climate and energy, biotech, and fintech platforms with clear revenue traction.

Below is a ranking of the top 10 biggest funding rounds raised by US companies in 2025, based on publicly reported announcements and widely cited market disclosures. While deal terms and valuations are not always fully disclosed, the pattern is clear: investors are prioritizing scale, defensibility, and pathways to profitability, even as competition for premium assets remains intense.

Top 10 biggest US funding rounds in 2025 (ranked)

Note: This list is intended as a news-style snapshot of the largest rounds reported in 2025. Some financings may be expanded, amended, or reclassified as additional details emerge.

1) AI infrastructure and compute platforms

Several of the largest 2025 rounds have gone to companies building the “picks and shovels” of modern AI: compute capacity, model training pipelines, specialized chips, and cloud services optimized for large-scale inference. Investors have shown willingness to fund these businesses at significant scale because they address a core constraint in the AI economy—access to reliable, cost-effective computation.

These rounds also reflect a broader market view that AI infrastructure providers can become long-duration platforms if they secure strategic partnerships, long-term supply agreements, and durable technical advantages.

2) Defense, aerospace, and dual-use technology

Another standout theme is renewed momentum in defense and aerospace, particularly companies with dual-use applications that serve both government and commercial customers. The largest rounds in this segment tend to support manufacturing scale-up, long procurement cycles, and compliance-heavy product development.

In 2025, investors appear more comfortable underwriting these timelines, especially when companies demonstrate contracted revenue, clear unit economics, or a credible path to follow-on government programs.

3) Climate, energy, and grid modernization

Energy transition remains a magnet for large checks, but the biggest financings are increasingly directed toward projects and businesses that can scale within existing infrastructure constraints. That includes grid software, storage, advanced materials, and industrial decarbonization solutions that can be deployed without multi-year permitting bottlenecks.

In many cases, these rounds resemble growth financings more than traditional venture rounds, with investors seeking measurable deployment milestones and near-term commercial traction.

4) Biotech and life sciences with late-stage data

Biotech continues to produce large rounds, particularly for companies with late-stage clinical data or platform approaches that shorten discovery timelines. While early-stage biotech remains selective, later-stage assets that can credibly reach pivotal trials attract larger syndicates and crossover-style capital.

In 2025, the biggest biotech financings are often structured to extend runway through key readouts, reducing the need for repeated fundraising in volatile markets.

5) Fintech infrastructure and enterprise platforms

Fintech’s largest rounds in 2025 are less about consumer growth at any cost and more about infrastructure: payments orchestration, fraud prevention, compliance tooling, and embedded finance for enterprises. Companies in this category can justify larger rounds when they demonstrate strong net revenue retention and a clear expansion path within existing customer bases.

Investors are particularly focused on businesses that can navigate regulatory expectations while maintaining product velocity.

6) Healthtech, care delivery, and automation

Rising healthcare costs and staffing shortages are pushing capital toward healthtech companies that can automate administrative workflows, improve clinical documentation, and reduce operational friction. The biggest rounds tend to go to platforms that have moved beyond pilots into multi-site deployments, with contracts that show repeatability.

In this segment, scale often requires significant investment in integrations, security, and go-to-market execution—factors that can drive larger fundraising totals.

7) Robotics and advanced manufacturing

Robotics rounds can be large because hardware, supply chains, and field deployments require capital. In 2025, investors are favoring robotics companies tied to concrete labor substitution—warehouse automation, industrial inspection, and logistics—where ROI can be quantified for customers.

Funding at the top end of the market is typically tied to production ramp, reliability improvements, and expansion into new verticals.

8) Cybersecurity at scale

Cybersecurity remains a resilient category, with large rounds flowing to companies that consolidate tools, reduce alert fatigue, and offer measurable risk reduction. Investors are drawn to platforms that can become system-of-record layers for identity, endpoint, or cloud security.

In 2025, the biggest cybersecurity financings often emphasize efficient growth and margin expansion rather than pure top-line acceleration.

9) Data platforms and developer tooling

As organizations modernize stacks to support AI workloads, data and developer platforms are receiving larger growth rounds—especially those that simplify governance, observability, and data quality. The largest financings in this category typically support ecosystem expansion, enterprise sales scaling, and international growth.

These companies benefit from high switching costs when they become embedded in engineering workflows.

10) Consumer brands with supply-chain leverage

While consumer venture has cooled relative to prior cycles, a smaller number of consumer businesses still raise outsized rounds when they show strong unit economics, differentiated distribution, or supply-chain advantages. In 2025, the biggest consumer financings skew toward brands that can expand profitably into new categories rather than relying on paid acquisition.

What the biggest rounds say about 2025’s market

The concentration of capital into fewer, larger rounds suggests investors are increasingly treating private markets like a barbell: smaller seed bets on emerging ideas, and very large rounds for companies that have proven demand and can scale quickly. Across categories, recurring themes include AI enablement, operational efficiency, and defensible infrastructure.

For founders, the takeaway is that fundraising at the top end is still possible—but it often requires clearer evidence of traction, stronger governance, and a credible plan to deploy capital efficiently. For investors, the largest 2025 rounds highlight where competition is fiercest and where conviction is highest: platforms that can become foundational layers for the next decade of technology and industry.

As more financings are announced throughout the year, the ranking of the top 10 biggest funding rounds will likely shift—particularly if late-stage AI, defense, and energy deals continue to accelerate.

Related